Gifted deposits feature in 8% of all residential property purchases

December 16, 2016- New analysis from My Home Move reveals rate of gifted deposits has increased by 1.6% to 8.1% over the last year, up from 6.5%

- Overall property purchases down 4% but home buyers using a gift rises 30%

- Gifted deposits even more prevalent among first-time buyers, with 17.1% of first-time purchases relying on a gift

- My Home Move predicts another seasonal spike in gifted deposits this Christmas

My Home Move, the UK’s leading provider of mover conveyancing services, has calculated that 8.1% of residential transactions included gifted deposits between November 2015 and October 2016 – up from 6.5% compared over the previous twelve months.

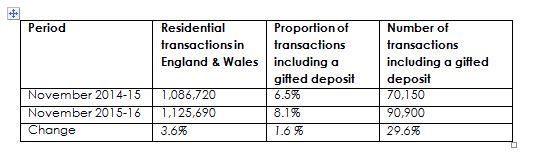

These findings mean that out of the 1.125 million residential property transactions recorded by HMRC over this period, an estimated 90,900 featured a gifted deposit, equating to over 20,000 more than in the previous twelve months.

Looking at the year before, between November 2014 and October 2015, My Home Move estimate that out of 1.086 million residential property transactions*, 70,150 included a gifted deposit. This means that while the overall number of residential transactions increased by just 3.6% year-on-year, the number featuring a gifted deposit jumped by 29.6%.

The findings illustrates the growing trend of family members and friends helping prospective buyers to raise a deposit. With house prices continuing to rise faster than incomes, My Home Move expects even greater numbers of gifted deposits in years to come.

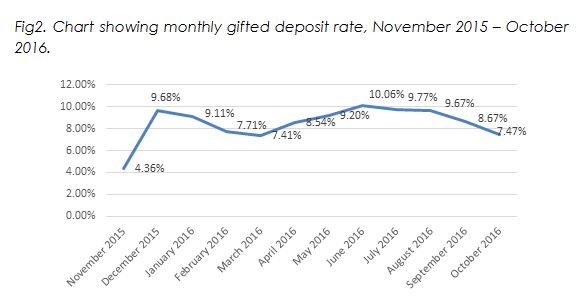

The analysis also reveals that the proportion of transactions featuring a gifted deposit fluctuated from month to month. In 2015, the proportion of completed transactions which included a gifted deposit jumped from 4.36% in November to 9.68% in December and 9.11% in January 2016, before tailing off again over spring and summer. The seasonal spike in completions means that for many a gifted deposit will feel like a great Christmas present, as they move into their new home.

First-time buyers more reliant upon gifted deposits

My Home Move’s analysis also reveals that the proportion of first-time buyers using a gifted deposit over this period was 17.1%. This is more than double the 8.1% observed among all homebuyers – illustrating the extent to which first-time buyers are reliant on friends and family members to get a foot on the housing ladder.

First-time buyers’ challenges are well known. According to the latest DCLG English Housing Survey (EHS), the average age of first-time buyers continues to rise as savers take longer to acquire the funds required for a deposit: over the last 20 years the average age of a first time buyer increased from 30 to 33 years. The EHS also reveals that couples now form the bulk of successful first-time buyers, with one income often no longer enough**.

The trend for the gifted deposit rate to rise over the festive period is also evident in the first-time buyer market. In late 2015, the rate of first-time buyers’ purchases including a gifted deposit jumped 8 percent from 12.9% in November to 20.9% in December.

Commenting on the findings, Doug Crawford, CEO of My Home Move, says:

“The impact of rising house prices on affordability has created a real challenge for first time buyers. Higher prices mean would-be first time buyers have to fund ever-larger deposits. House prices rising faster than incomes can make saving up a challenge for even relatively affluent buyers. Properties in in-demand areas can require enormous deposits, and buyers are not helped by high rental costs.

“Many parents are therefore happy to help their children out with money towards a deposit. A property purchase gives young people the opportunity to build up a solid amount of equity over a number of years and offers stability. With property prices racing ahead of earnings, we’re expecting to see the gifted deposit rate surpass the 10% mark soon. However, a large-scale reliance among first-time buyers on gifted deposits is unsustainable; and so it is important that those without the luxury of a gift from family and friends can get on the ladder, if the market is to work for everyone.

“The widespread use of gifted deposits is not limited to first-time buyers. A gifted deposit can significantly reduce mortgage costs by enabling buyers to access much more attractive rates by borrowing less. For young families looking to move to a bigger property, help from mum and dad can make a big difference.”

My Home Move’s top tips on giving or receiving a gifted deposit

1. Inform your conveyancer – as soon as your offer is accepted, ensure the conveyancer is aware that some or all of the deposit is a gift.

2. Provide evidence that the money was a gift and not a loan – when giving a gifted deposit, the lenders will need written consent – often as a letter or part of a form – confirming the money was a gift and the provider has no personal interest in the property.

3. Ensure you have the right proof of identification – this may sound simple, but quite often photocopies of ID will not be accepted by a solicitor. This can become problematic if the person giving the gift is either overseas or unavailable.

4. Have the necessary bank statements at the ready – part of the process involves anti-money laundering checks which includes checking bank statements from the person giving the gift and the recipient, to confirm that the money was earned legitimately.

5. Understand what a gifted deposit means for you – most importantly, if you are the contributor of a gifted deposit, you must be aware that once you complete the process, you no longer have any rights to the money or the property.